Meta Description: Learn startup accounting fundamentals, essential tools, and best practices to manage finances, avoid costly mistakes, and stay investor-ready from day one.

Introduction

Running a startup is exhilarating—until cash flow problems derail your dreams. Here’s a sobering statistic: 82% of failed ventures collapse due to poor cash flow management, not because their product was bad.

The difference between startups that thrive and those that struggle often comes down to one critical factor: financial discipline from day one. Yet many founders treat accounting as an afterthought, relegating it to spreadsheets or hiring accountants “when they can afford it.”

This guide cuts through that noise. Whether you’ve just incorporated or you’re pre-revenue, this is your complete blueprint for startup accounting—covering essential tools, must-know best practices, common pitfalls to avoid, and actionable strategies to keep your startup financially healthy.

Startup founder managing finances with accounting software on desk

Understanding the Startup Accounting Fundamentals

Before diving into tools or strategies, every founder needs to understand what “startup accounting” actually means—and why it’s different from traditional business accounting.

What Is Startup Accounting?

Startup accounting is the practice of tracking, organizing, and reporting a company’s financial activity in a way that supports decision-making, compliance, and fundraising. Unlike established businesses with predictable revenue, startups typically operate in survival mode—burning cash while hunting for product-market fit. This reality demands a different accounting approach.

The Three Essential Financial Statements Every Founder Must Know

Your financial health is told through three interconnected statements:

1. Income Statement (P&L)

Shows whether your startup is profitable over a period. It tracks revenue minus expenses to reveal net income or loss. For SaaS startups, this is where revenue recognition mistakes happen—recording an annual subscription upfront instead of spreading it over 12 months violates GAAP standards.

2. Balance Sheet

A snapshot of what your startup owns (assets), owes (liabilities), and owner equity. This matters when raising capital—investors scrutinize your balance sheet to understand your asset base and debt obligations.

3. Cash Flow Statement

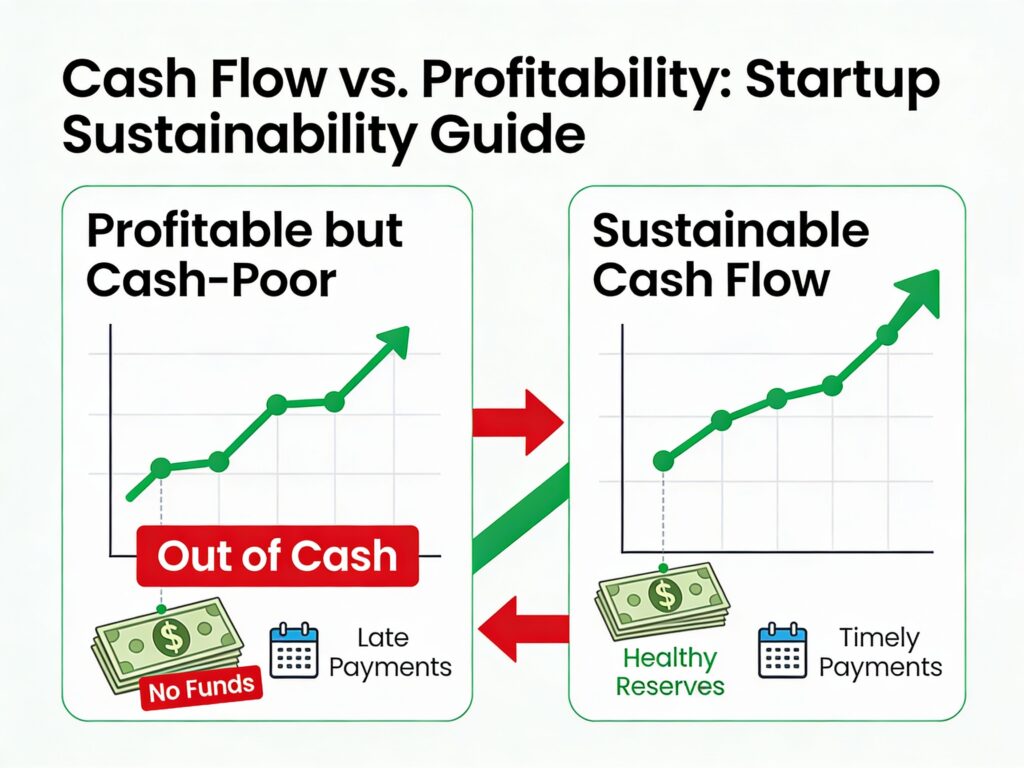

The most important statement founders ignore until it’s too late. Cash flow shows the actual movement of money in and out of your business. A company can be profitable on paper yet run out of cash if customers pay late or expenses are front-loaded.

The Critical Insight: Profitability ≠ Cash Flow. You can be profitable and still run out of money. You can be unprofitable and have plenty of cash (common with venture-backed startups). The 2026 startup that understands this distinction survives.

Understanding Cash Flow vs Profitability in Startups

The 5 Critical Mistakes Startups Make (and How to Avoid Them)

Learning from others’ errors is faster than making them yourself. Here are the five accounting mistakes that derail founders most often—and the exact fixes.

Mistake #1: Mixing Personal and Business Finances

The Problem: Using your personal bank account for business expenses or swiping your personal credit card “just once” is the #1 path to accounting chaos. It creates a nightmare during tax time, raises red flags with investors, and makes audits a disaster.

The Fix: Open a dedicated business bank account and credit card on day one—literally before you incorporate. Separate accounts take 20 minutes and save weeks of cleanup later. Never, ever mix personal and business money.

Pro Tip: Use a startup-friendly bank like Mercury, Brex, or Wise that offers good integrations with accounting software and basic spend controls.

Mistake #2: Failing to Reconcile Accounts Monthly

The Problem: Without monthly reconciliation (matching your accounting records to bank statements), errors snowball. A duplicate transaction, a missed expense, or a payment recorded twice goes unnoticed until it’s too late.

The Fix: Reconcile your bank and credit card accounts every month. Most accounting software automates 80% of this work—you just review and confirm. Schedule a 30-minute session on the 5th of each month (after all transactions have cleared).

Mistake #3: Misclassifying Expenses (Especially for SaaS)

The Problem: Lumping software subscriptions, cloud hosting, and developer tools into a single “Miscellaneous Expense” category destroys visibility. You can’t see where your money’s actually going, and you’ll miss deductions at tax time.

The Fix: Build a detailed chart of accounts tailored to your business model. For SaaS startups, separate accounts should include: Hosting & Infrastructure, Software Subscriptions, Customer Support, R&D Labor, and Customer Acquisition. Review categories quarterly and refine.

Mistake #4: Not Using Accounting Software (Spreadsheets Are a False Economy)

The Problem: “We’ll just use Google Sheets for now” is a lie every founder tells themselves. Spreadsheets are error-prone, don’t scale, and waste 10+ hours per month on manual data entry. More critically, they make it impossible to track real-time cash position.

The Fix: Choose cloud accounting software within your first 90 days of operation. For most startups, QuickBooks Online ($25/month) or Xero ($13/month) are perfect starting points. Wave is free if budget is absolutely constrained, but the time savings of paid software justify the cost immediately.

Mistake #5: Booking Equity Investments as Revenue

The Problem: Recording a SAFE note, seed round, or convertible note as “revenue” on your income statement is a critical error that makes your numbers meaningless. It overstates profitability and triggers IRS scrutiny.

The Fix: Equity funding belongs on your balance sheet as a liability (initially) or equity, never on the income statement. Consult your accountant on how to record convertible instruments correctly.

5-Step Accounting Setup Process for New Startups

Your Complete Accounting Setup Checklist

Here’s the exact order to set up accounting for your startup, whether you’re pre-revenue or already generating sales:

Phase 1: Foundation (Do This First)

- Incorporate your startup (LLC, C-Corp, or S-Corp)

- Open a dedicated business bank account

- Get an EIN from the IRS (free, takes 15 minutes online)

- Open a business credit card (ideally with accounting integrations)

- Maintain a chart of accounts specific to your business model

- Set up separate folders for invoices, receipts, and tax documents

Phase 2: Systems (Weeks 1-4)

- Choose and implement accounting software (QuickBooks, Xero, or Wave)

- Connect your bank account for automated transaction syncing

- Set calendar reminders for monthly reconciliation (1st of each month)

- Establish approval workflows for expenses over $500

- Create a digital receipt storage system (Expensify, Wave, or Google Drive)

- Document your bookkeeping process in a 1-page playbook

Phase 3: Ongoing Operations (Monthly)

- Review and categorize all transactions

- Reconcile bank and credit card accounts

- Send invoices to customers within 24 hours of delivery

- Approve vendor payments

- Review cash position weekly

- Generate P&L, Balance Sheet, and Cash Flow reports

Phase 4: Compliance (Quarterly & Annually)

- Prepare quarterly tax estimates (if applicable)

- Review financial statements with your accountant

- Monitor burn rate and runway

- Collect 1099 forms from contractors before year-end

- File annual tax returns

The Best Financial Tools for Startup Accounting in 2026

Choosing the right tool is critical—it’s the foundation of your financial operations. Here’s how to pick:

For Early-Stage Startups (Pre-Revenue to $10K MRR)

Recommendation for you: Start with Xero or QuickBooks Online. They’re industry standards—any accountant will work with them, they integrate with most fintech tools, and they scale from $0 revenue to $10M+.

For Growth-Stage Startups ($10K-$100K MRR)

Once you’re generating meaningful revenue and potentially hiring, upgrade to:

- Xero + Brex (spend management) + Gusto (payroll)

- QuickBooks Online + Stripe (payment integration) + Rippling (HRIS)

- NetSuite (if you need enterprise-grade capabilities and have raised Series A)

Pro Tip: A 75% of cloud accounting users saw an increase in profit versus 54% of non-cloud users. The software pays for itself through visibility and automation.

Master Your Cash Flow: The #1 Reason Startups Fail

Cash flow is the nervous system of your startup. Here are the non-negotiable practices that keep it healthy:

1. Forecast Your Cash Flow Weekly, Not Just Monthly

Most startups review cash flow monthly—too late to catch problems. Instead, create a rolling 13-week cash flow forecast that updates weekly. Track:

- Expected customer payments (invoice by invoice)

- Known expenses (payroll, rent, software subscriptions)

- Variable costs tied to growth

- Tax liabilities (quarterly estimates)

Tool: Use Planguru ($99/month) or a simple spreadsheet template. Update it every Friday. Review with your co-founder or advisor.

2. Build a Cash Reserve Before You Need It

Financial advisors recommend maintaining 3-6 months of operating expenses in reserve. For a startup burning $50K/month, that means $150K-$300K in savings.

Early on, when you don’t have this cushion, prioritize:

- Cutting non-essential expenses (SaaS tools, nice-to-haves)

- Accelerating customer payments (offer 2% discount for payment within 7 days)

- Negotiating extended payment terms with vendors (net-60 instead of net-30)

3. Track Weekly Cash Position

Every Monday morning, spend 10 minutes knowing:

- Current cash in bank

- Expected customer payments coming in (next 4 weeks)

- Committed expenses going out (next 4 weeks)

- Runway in weeks (cash balance ÷ weekly burn rate)

This single practice catches cash emergencies before they become death spirals.

4. Optimize Accounts Receivable

Delayed customer payments are the #1 cash flow killer. Fix this by:

- Invoicing immediately after delivery (not end of week)

- Offering a 2% discount for payment within 7 days

- Setting clear payment terms (Net-15, not Net-30)

- Following up on overdue invoices within 2 days (template: “Hi [Name], just confirming receipt of invoice [#] for $[amount], due [date].”)

- Using automated payment reminders (FreshBooks, Xero, QuickBooks)

Impact: Shortening payment cycles by just 10 days can unlock $50K+ in cash for a $500K/year startup.

5. Maintain a Spending Discipline (Budget + Rules)

- Set monthly expense budgets by category (payroll, marketing, cloud hosting, etc.)

- Require approval for any expense over $500 (or 5% of monthly revenue)

- Review spending weekly to spot unusual patterns

- Negotiate vendor rates quarterly—many SaaS companies offer discounts for annual commitments

Key Financial Metrics Every Founder Must Track

Beyond P&L and cash flow, these metrics reveal your startup’s true financial health:

| Metric | Formula | Why It Matters |

|---|---|---|

| Burn Rate | (Cash Spent – Revenue) / Month | How many months until you run out of cash |

| Runway | Cash Balance / Monthly Burn Rate | Your survival timeline |

| Monthly Recurring Revenue (MRR) | Predictable monthly revenue (SaaS/subscriptions) | Revenue quality and growth trajectory |

| Cash Conversion Cycle | Days to convert expense → cash back | How efficiently you turn investments into revenue |

| Customer Acquisition Cost (CAC) | Marketing Spend / New Customers | Unit economics of your growth |

| Gross Margin | (Revenue – COGS) / Revenue | Profitability potential per customer |

Track these in a simple Google Sheet or use a financial dashboard tool like Planguru. Share with your co-founder and board monthly.

Tax Compliance: Don’t Get Caught Off Guard

Even pre-revenue startups have tax obligations. Founders who ignore this end up with penalties:

Startup Founders Must File These:

- Estimated Quarterly Taxes (if projecting $1,000+ profit for the year)

- Payroll Taxes (withholding, FICA, unemployment insurance—if you have employees)

- Sales Tax (if required in your jurisdiction or selling taxable goods)

- Annual Income Tax Return (federal and state)

You May Qualify For These Credits:

- R&D Tax Credit (if your startup develops software, hardware, or processes)

- Employee Retention Credit (ERC) (if you raised funding during pandemic)

- Work Opportunity Tax Credit (if hiring from eligible populations)

Action: Consult a startup accountant (like Kruze Consulting, Founders CPA, or Smart Accountants) before year-end to identify available credits. Many startups leave $20K-$100K on the table.

Your Roadmap to Investor-Ready Financials

If you’re raising capital, your financial statements become your credibility. Here’s what investors expect:

Due Diligence Checklist:

- 3 years of tax returns (or since incorporation)

- Monthly P&L, Balance Sheet, and Cash Flow for past 2 years

- Cap table showing all equity holders and vesting schedules

- Bank statements and reconciliations (past 6-12 months)

- Customer contracts and revenue recognition documentation

- Debt agreements and borrowing obligations

- Lease agreements for office/equipment

- Employee offer letters and equity documents

Pro Tip: Keep this documentation organized and digital from day one. When due diligence comes, you’ll be ready in hours instead of weeks.

Frequently Asked Questions (FAQs)

Q: When should I hire a bookkeeper or accountant?

A: Hire a bookkeeper when one of these happens:

- You raise external capital from investors

- You hire your first employee

- You generate $10K+ monthly revenue

Until then, use accounting software + a part-time accountant (5-10 hours/month for review) to keep costs low.

Q: Cash or Accrual Accounting—Which Should I Use?

A: Most startups use accrual accounting (record revenue when earned, expenses when incurred). This is required by GAAP standards and expected by investors. Cash accounting (record only when money moves) is simpler but inaccurate for startups with receivables or vendor terms.

Consult your accountant, but default to accrual.

Q: What’s the difference between a bookkeeper and a CPA/accountant?

A:

- Bookkeeper: Records daily transactions, reconciles accounts, prepares financial statements. Cost: $1K-$3K/month

- CPA/Accountant: Reviews bookkeeper work, files taxes, provides strategic advice (burn rate analysis, fundraising prep). Cost: $3K-$10K+/month

Most startups use a bookkeeper (internal or outsourced) + quarterly accountant reviews.

Q: My books are a complete mess. How do I recover?

A: Hire a bookkeeper to do a “cleanup engagement”—they’ll:

- Reconcile all historical transactions

- Categorize expenses correctly

- Adjust entries for errors

- Generate accurate financial statements

Cost: $2K-$10K depending on the mess. Time: 4-8 weeks. Then start fresh with clean books and proper systems.

Q: Do I need a separate business entity (LLC vs. C-Corp)? Does it matter for accounting?

A: Yes, it matters hugely.

- LLC: Pass-through taxation (simpler accounting, but may not attract venture capital)

- C-Corp: Separate corporate taxes (more complex accounting, required for VC funding)

- S-Corp: Tax-efficient hybrid (complexity increases, suited for profitable startups)

For venture-backed startups, use a C-Corp. For bootstrapped/consulting businesses, an LLC often makes sense. Consult a startup lawyer (costs $500-$1,500) to pick the right structure—the accounting implications are significant.

Q: What accounting software integrations matter most?

A: Prioritize integrations with:

- Your bank (automatic transaction syncing)

- Invoicing/payment (Stripe, PayPal, Square)

- Payroll (Gusto, Rippling)

- Expense management (Brex, Ramp)

- Investor reporting (Carta, Pulley for cap table)

QuickBooks and Xero both offer 1,000+ integrations. Ensure your chosen software connects to your critical tools.

Q: How often should I review my financials?

A:

- Weekly: Cash position and burn rate (10 minutes)

- Monthly: Full P&L, Balance Sheet, Cash Flow (1-2 hours with your accountant or bookkeeper)

- Quarterly: Strategic review with board/advisors (discussion of burn, runway, fundraising needs)

- Annually: Tax preparation and financial audit (if raising capital)

Startups that review only quarterly are flying blind. Make this a weekly ritual.

Q: Is it cheaper to DIY accounting or outsource?

A: For the first 18-24 months, DIY + quarterly reviews is cheapest:

- Accounting software: $25-150/month

- Quarterly accountant review: $500-1,500

- Total: $3K-$5K/year

Once revenue exceeds $50K/month or you hire employees, outsource to a bookkeeper ($1K-$3K/month). The tax savings and operational clarity justify the cost.

Q: What documentation should I keep forever?

A: The IRS requires you keep records for 3-7 years depending on the type:

- Bank statements & reconciliations: 7 years

- Tax returns: 7 years (indefinitely recommended)

- Invoices & receipts: 3-7 years

- Payroll records: 4 years

- Contracts & agreements: 3-7 years (or length of agreement + 3 years)

Best practice: Keep everything in a cloud-backed system (Google Drive, Dropbox) indefinitely. Digital storage is cheap; missing documentation during an audit is expensive.

Your Action Plan: This Week

Feeling overwhelmed? Here’s what to do in the next 7 days:

Day 1-2: Open a business bank account. (Time: 30 minutes)

Day 3: Choose your accounting software. Free trial QuickBooks or Xero. (Time: 1 hour)

Day 4: Set up your chart of accounts. Download a template for your industry. (Time: 2 hours)

Day 5: Connect your bank account to your software. Start categorizing transactions. (Time: 1 hour)

Day 6: Schedule monthly reconciliation. Set a recurring calendar reminder for the 5th of each month. (Time: 15 minutes)

Day 7: Hire a part-time accountant for quarterly review. Post a job on Upwork or ask your network. (Time: 2 hours)

That’s it. One week to financial clarity.

Conclusion

The founders who succeed aren’t necessarily the smartest—they’re the ones who obsess over cash flow and maintain clean books. Accounting might seem like a boring, back-office function, but it’s the nervous system of your startup.

Clean accounting gives you:

- Real visibility into your business (where money actually goes)

- Ability to raise capital (investor-ready financials)

- Confidence to make decisions (data-driven, not guesses)

- Sleep at night (no tax surprises or compliance nightmares)

Start this week. Open the bank account. Pick the software. Schedule the monthly reconciliation.

Your future self—the founder who just closed Series A or hit profitability—will thank you.